How Clean Books Make Bank Loans and Financing Easier to Secure

Clean books make it easier to secure bank loans and financing because lenders rely on accurate, organized financial records to assess risk.

When your books clearly show cash flow, profitability, and liabilities, lenders can quickly understand your business and move forward with confidence. When records are messy or incomplete, approvals slow down or stop entirely.

Lenders are not just funding ideas; they are funding clarity, consistency, and reliability. Your bookkeeping plays a direct role in how easy or difficult that process becomes.

Why Do Lenders Care So Much About Clean Books?

Lenders care about clean books because financial statements are how they verify your ability to repay a loan. Your books tell the story of how money moves through your business over time.

When records are accurate and up to date, lenders can see patterns. They can evaluate risk without guessing, which reduces hesitation.

When books are disorganized, lenders see uncertainty; this uncertainty often leads to more questions, delays, or rejection.

Clean books show lenders:

- Consistent revenue

- Predictable expenses

- Real cash flow, not estimates

- Accurate liabilities and debt levels

- Proper separation of business and personal finances

If your reports raise questions, lenders will pause. If they answer questions upfront, lenders move faster.

What Financial Documents Do Lenders Review?

Lenders review a short list of core documents to assess your financial health. Clean books make these documents accurate and easy to produce.

Most lenders request:

- Profit and loss statements

- Balance sheets

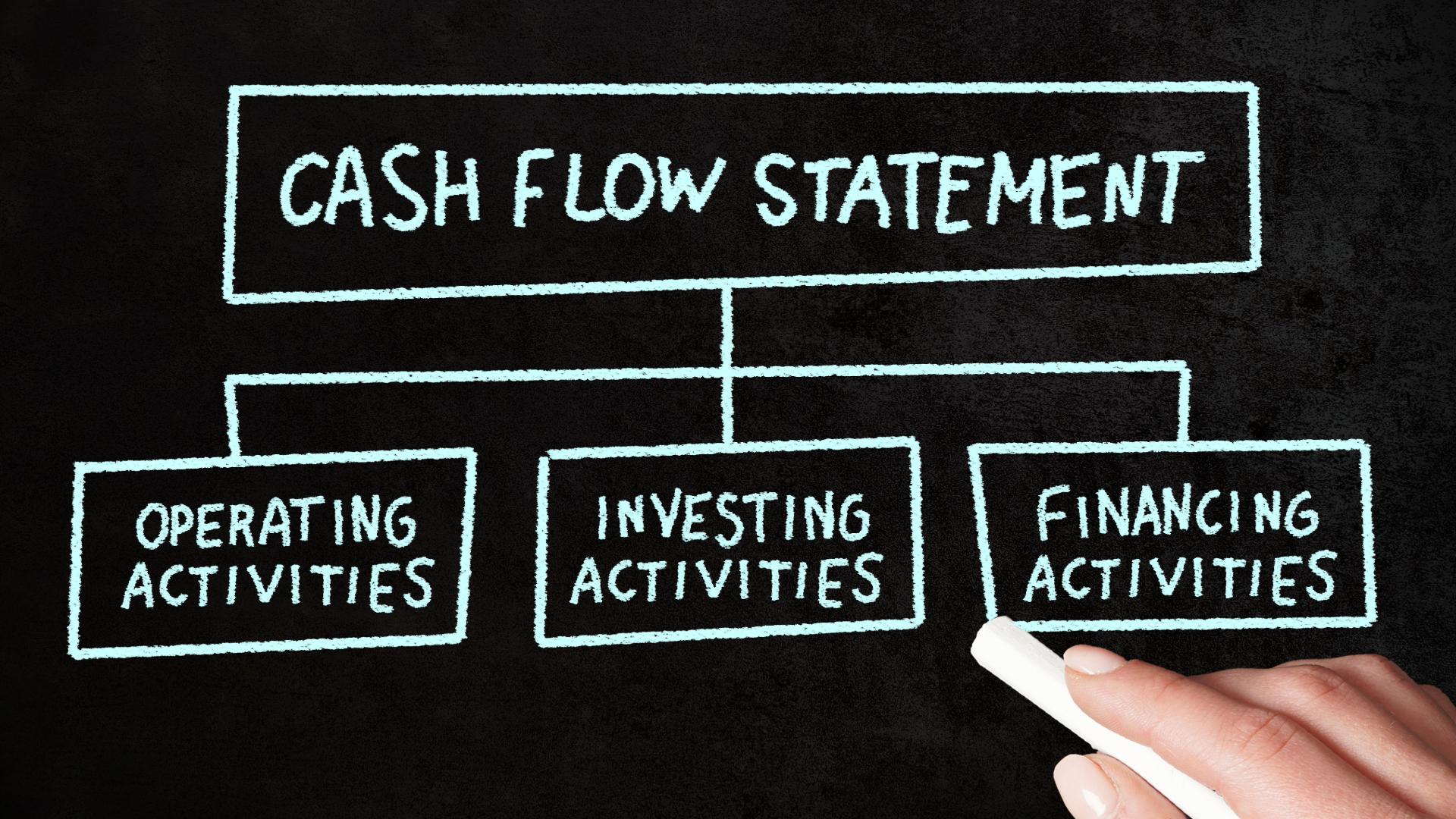

- Cash flow statements

- Accounts receivable aging

- Accounts payable aging

- Recent tax returns

If these reports tell different stories, lenders notice. For example, a profit and loss statement that shows high income but a cash flow statement that shows frequent shortages signals risk.

Clean bookkeeping ensures those reports align.

How Do Messy Books Delay or Block Loan Approvals?

Messy books delay approvals because lenders cannot trust what they see. When numbers do not reconcile, lenders ask for clarification, ultimately creating a back-and-forth that drags out the process.

Common issues include:

- Unreconciled bank accounts

- Missing transactions

- Inconsistent expense categorization

- Owner draws mixed with operating expenses

- Outdated reports

Imagine applying for a loan to purchase equipment. The lender requests financial statements for the last 12 months.

Meanwhile, your bookkeeper has not reconciled the accounts for three months, and the reports change every time new data is added. The lender now must wait for corrections before proceeding.

That delay can ultimately cost you your opportunity.

How Do Clean Books Reduce Lender Risk?

Clean books reduce lender risk by proving your numbers are reliable. Accurate bookkeeping shows that your business operates with discipline and control.

Lenders assess risk by asking the following:

- Can this business repay the loan?

- Is cash flow stable enough to support debt payments?

- Are expenses under control?

- Does management understand the numbers?

Clean books help answer all these questions without explanation.

When lenders feel confident in your reporting, they are more likely to:

- Approve financing

- Offer better interest rates

- Borrow larger amounts

- Structure more flexible terms

How Does Cash Flow Clarity Impact Financing Decisions?

Cash flow clarity directly affects whether a lender believes you can make payments on time. Profit alone does not guarantee repayment.

Your cash flow statement shows:

- When money enters the business

- When money leaves the business

- Periods of tight cash

- Timing gaps between receivables and payables

Clean books make cash flow timing visible. That matters because many businesses fail loan reviews, not because of a lack of profit, but because of cash flow strain.

For example, a construction company may be profitable on paper but struggle with delayed client payments. Without accurate accounts receivable tracking, lenders see risk.

Clean books make that timing transparent and manageable.

Why Consistency Matters More Than Perfection

Lenders do not expect flawless finances. They expect consistency.

Clean books show these consistent processes in the form of:

- Monthly reconciliations

- Standard expense categories

- Regular financial reporting

- Clear documentation

Inconsistent books raise red flags, even if the numbers look good. A sudden jump in expenses or unexplained revenue changes prompt questions.

Consistency signals stability. Stability supports trust.

What Role Does Bookkeeping Play Before You Apply for Financing?

Bookkeeping plays the most important role before you apply for financing. Waiting until a lender asks for documents puts you on defense.

Preparing early puts you on offense.

- Fix categorization issues

- Clean up owner transactions

- Address outstanding receivables

- Reconcile accounts

- Review trends proactively

When a lender asks for reports, you should already have them ready. Clean books turn loan preparation into a submission, not a scramble.

How Far Back Do Lenders Look at Your Books?

Most lenders review at least twelve months of financial activity. Some reviews are 2 to 3 years, especially for larger loans.

Clean books over time show trends, not just snapshots. Lenders want to see how your business performs during slow periods, seasonal fluctuations, and growth phases.

Incomplete records limit that visibility and weaken your application.

What Does Having "Clean Books" Mean to a Lender?

To a lender, "clean books" are less about sophistication and more about trust. They want to see financials that clearly reflect how your business operates, how stable it is, and how responsibly it's managed.

When your records are accurate, consistent, and easy to verify, lenders can assess risk quickly and with confidence.

To a lender, having clean books mean:

- All bank and credit card accounts reconciled

- Accurate profit and loss statements

- Balance sheets that balance

- Clear separation of business and personal finances

- Up-to-date accounts receivable and payable

- Consistent expense categorization

- Documentation that supports reported figures

Clean does not mean complex. It means accurate, organized, and reliable.

Connect With N.E.W. Accounting

At N.E.W. Accounting, we help business owners maintain clean books that support growth decisions, not just compliance. That includes preparing financials that stand up to lender review and clearly reflect your business performance.

If financing is part of your future, your books should support that goal now. Clean books give you leverage, clarity, and confidence before you sit across from a lender.

When your numbers tell a clear story, lenders listen

If you are planning to apply for a loan, line of credit, or other financing, your books should work for you, not against you.

Contact our team today to get your books financing-ready and move forward with confidence.